Hello Readers!

How are you all? Well, on 1st February 2020 that is on last Saturday, our honorable Finance Minister, Smt. Nirmala Sitharaman announced our India Budget for the financial session 2020-21.

Seeing the economic slowdown in the Indian market, people were expecting a strong financial budget, that would effectively revive the slowdown of the economy in less time. The budget presented by the finance minister has many good key points, and predominantly it was incremental in nature, however, it lacked the measures for the fast revival of the economy.

It is a must to know what the good points of the Indian Budget for the fiscal year are 2020-21, and what it has for its public welfare. Here we are going to discuss the key highlights of the Indian Budget for the financial year 2020-21 and what it has for you, read to know about it:

KEY HIGHLIGHTS

1. FY21 Fiscal deficit estimated at 3.5%; Escape clause invoked in FY20:

Lower collection of GSTs (Goods and Services Tax) than expected and reduction in corporate tax rates have affected the government tax collection. Thus, the government has revised the current year's Financial shortfall target to 3.8% which was earlier 3.3%.

The finance minister used the ‘escape clause’ under the FRBM Act (which allows leeway to relax the fiscal deficit target by up to 0.5%). The financial shortfall target for the fiscal year 2020-21 has been fixed to 3.5% in line with market expectations, also the nominal GDP (Gross Domestic Product) growth for the fiscal year 2020-21 has been estimated to 10%.

2. Ambitious Disinvestment target – LIC IPO remains the key

The disinvestment target for the financial year 2020-21 has been increased to ₹ 2.1 Lakh crore, which was originally set to ₹ 1 lakh Crore for the financial year 2019-20, that later was revised sharply downward to ₹ 65, crores. The government has planned to sell a part of their holdings of LIC (Life Insurance Corporation) via an IPO (Initial Public Offering) and some of its stakes of IDBI bank, in order to bridge the revenue shortfall, but the point is this will work only if we have a buoyant market.

3. Corporate Tax proposals bring cheer

- Lower corporate tax rates of 15%, that was introduced in September 2019, for new manufacturing companies, now includes newly incorporated power generation companies, that will start their production till 31st March 2023.

- Earlier, the start-ups with a turnover up to ₹25 crores were allowed for a deduction of 100% of their profits for 3 consecutive years out of seven, whereas as per the financial budget for the fiscal year 2020-21, the start-ups with a turnover up to ₹100 crores will be allowed for a deduction of 100% of their profits for 3 consecutive years out of 10 years.

- Cooperative societies will now be taxed at 22% plus 10% surcharge and 4% cess with no exemption/deductions, as per the financial budget for the year 2020-21. Earlier cooperative societies were taxed at a rate of 30% with surcharge and cess.

- Businesses or companies with a turnover of fewer than 5 crores (earlier 1 crore) don’t have to get their books of accounts audited by an accountant. This eases their compliance burden. However, the higher limit will only apply to those businesses, that have less than 5% of their business transactions in cash.

4. Attracting foreign Investors

Well, the government has taken major steps to increase the interest of foreign investors in the Indian Market. FPI (Foreign Portfolio Investment) limit in corporate bonds has been raised from 9% to 15%.

Also, Sovereign Wealth Funds will be granted 100% tax exemption on interest, dividend and capital gains in respect of investments made in infrastructure and other notified sectors before 31st March 2024 and with a minimum lock-in period of 3 years.

What It Has for You As An Investor?

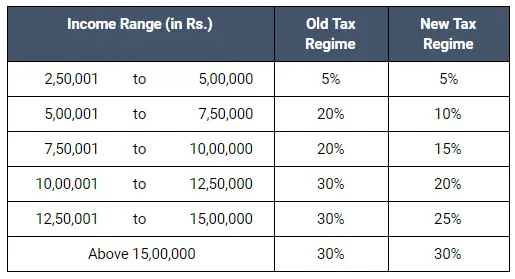

1. Lower Income Tax Rates for Individuals.

The new tax rates will be applicable to those who go without exemptions and deductions. The deductions include Standard deduction, Section 80C, Section 80D, LTA, HRA, interest on housing loan on the self-occupied property among others.

However, the new rates will be optional, that is individuals, as per their choice can opt for the new tax and slab rates, while they can continue with the old tax rates and slabs.

Individuals will have to check if they will have a greater benefit under the new tax rates and decide on which option to choose.

2. More Safety to Bank Depositors – Bank Deposit insurance hiked to ₹5 lakhs

Well, those who prefer to keep deposits in the banks, here is good news for you. Insurance cover on bank deposits has been raised from ₹1 lakh to ₹5 lakh, in case of bank failures. Also, if you have deposits in more than one bank, the insurance coverage limit applies separately to the deposits in each bank.

3. Dividend Distribution Tax – Burden transferred to investors

Stocks: Dividend Distribution Tax (DDT) that is currently paid by the companies, of around 20.56% (including cess and surcharge) on their aggregate dividends, however, as per the financial budget for 2020-21, these will now be taxed in the hands of the recipient as per his/her personal income tax slab.

Well, this is not good news for those who come under high-income tax slab, at the same time this will also increase the attention of foreign investors as they will be subject to the lower dividend tax rate applicable to them under various tax treaties.

Mutual Funds: Dividend paid by mutual fund schemes to its investor will also be liable for the tax deduction, in the hands of the investor at his applicable income tax slab rate.

Current tax rates on the dividend are 11.648% on equity schemes and 29.12% on debt schemes.

Also, dividends over ₹5,000 a year will be subject to a 10% tax deduction in the case of Indian investors, whereas dividends received by NRIs (Non-Resident Indian) will be subject to a 20% tax deduction irrespective of the dividend amount.

4. High earners to shell out more in Employer’s contribution to EPF

As per the financial budget for the fiscal year 2020-21, now employer contributions to a recognized provident fund, superannuation fund and NPS (National Pension Scheme), beyond ₹7.5 lakhs a year in total will be subject to tax, that is the benefits earned will be taxable.

5. Segregated Portfolio of Debt Mutual Fund to tax you less

Investors who have a segregated portfolio, the period of holding and proportionate cost of the main portfolio will be available for the segregated portfolio.

6. Residency Test – NRIs not taxed in any country will pay tax in India

An Indian Citizen will now be considered a resident of India and will be taxed accordingly on his income generated in India if he is not liable to pay tax in any other country. Also, the government announced that incomes generated outside of India will not be taxed, until and unless it is derived from an Indian business or profession.

The parameter to be categorized as NRI has also been changed, now an Indian has to stay abroad for 240 days to be considered as NRI, and an Indian who wants to claim the non-resident status can’t stay in India for more than 120 days or more in a year.

7. Introduction of Debt ETF

Post the success of the Edelweiss Bharat Bond ETF, the government will launch another ETF to raise money.

Equity Market Perspective: Expectation mismatch

There was an expectation of some strong reforms announcements to revive the current economic slowdown, which was seen missing in the financial budget. Also, there was no announcement regarding the lowering of LTCG (Long Term Capital Gains Tax) inequities.

This budget has indicated its purpose to move in long term growth, and thus we continue to recommend patient long term investors to stick to their long term asset allocation and not get afraid by the near term volatility.

Debt Market Perspective: Near Term Positive

The decision taken to increase FPI limit in corporate bonds from 9% to 15% of the outstanding stock of corporate bonds will help improve the liquidity in bond markets and most importantly, opening up of certain categories of government securities for NRI investors to invest is also a step in this direction.

Also, other factors such as moderation of global growth, softening global commodity prices, easing stance of major global central banks, slowing domestic growth, weak credit growth and high real yields in India also point towards lower yields.

Whereas on the negative side, excess SLR (Statutory Liquidity Ratio) investments within the banking system and high food inflation remain the key risks that still need to be monitored.

However, we still recommend our debt investors, to remain stuck to their debt funds with high-quality credit and with short duration (less than 3 years).

You can contact us at Shri Ashutosh Securities Pvt Ltd., for any further detail or information, we are here to help you in any way possible.

Happy Investing!

(Mutual Fund investments are subject to market risk Illustrations are for example only, there is no guarantee of returns. Past performance is not an indicator/guarantee to future returns).