Hello Readers!

Retirement, a phase of an individual life, where he has monthly expenses to cover but no income source to get money for those expenses. And this is why every individual’s very first goal is to plan their after retirement expenses while they are working.

In the country the general age to retire for every individual is 60 years, however, the age is only not the factor that decides how much ready you are to retire. Instead how much you have prepared yourself financially to retire is the factor that decides when you should retire! One can retire earlier too, provided it has saved enough for the rest of its life.

What Expert Say?

Experts say individuals must prepare themselves financially before they plan to retire so that they can easily combat theirs after retirement expenses. As per tax and investment experts, if an individual wants to retire early, he or she will have to start investing as early as possible or say at least by 25 years of age. They further added that investing through SIP (systematic investment plan) in mutual funds for the long term is something that will help them accumulate whopping amounts with small monthly investments.

In fact, in case you are not looking for early retirement but retirement at the age of 60 years, that also you must start planning your retirement expenses as early as possible to create a good retirement wealth.

How To Start Planning For Retirement?

Well, the very simple way to start planning for your retirement is by starting with calculating your retirement expense estimate. While you calculate your retirement expense, before that analyze your retirement years, how much long-lasting it could be.

Advancement in science and technology has led to an increase in the average lifespan of humans. So basically, you would have to plan your retirement expenses for around 25-30 years.

Before you calculate your retirement expense for around 25-30 years, first fix what kind of lifestyle you would be living in your retirement days. Will it be a modest daily life or one that will involve a high standard of living? After you analyze all these things, you would easily calculate your retirement corpus.

How To Build A Corpus Of Rs 5 Crore By Age Of 50?

SEBI registered tax and investment expert Jitendra Solanki said, "To create ₹10 core retirement corpus by age of 50 requires financial discipline, and investment planning at the early phase of one's career is a must. If a person wants to retire by 50 years of age, then he or she will have to start investing for retirement fund by 25 years of its age”.

That simply means, to create this big corpus you need to start investing at the age of 25. This is obvious that investing a huge lump sum amount at the age of 25 is much difficult as this is just the start of your career. However, with SIP is a Systematic Investment Plan, you do not need a big sum of money at once, instead, a small amount at regular intervals say monthly.

Well, to achieve this much big corpus, SIP alone may not help you reach that, so what is the way? SIP step up is the way that will help you achieve this big amount! A person's income is expected to grow annually and hence one should think of increasing one's investments too. So, a 10 percent annual step-up in monthly SIP will help the investor reach the ₹5 crore target

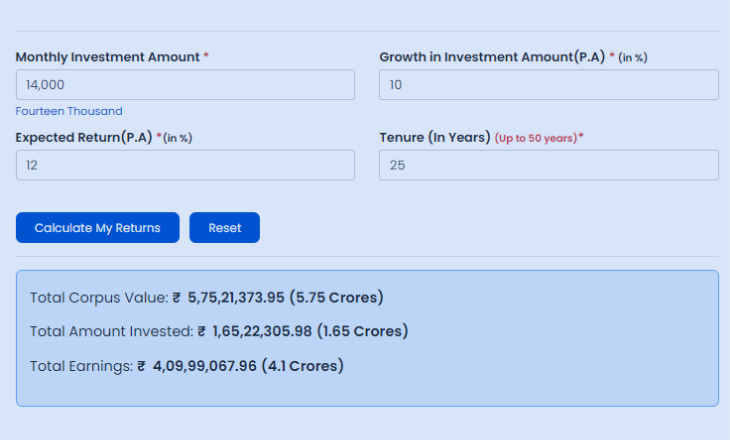

As per the mutual fund SIP calculator, if a person starts SIP at the age of 25 assuming 12 percent annual return and ₹5 crore investment goal in focus when he or she turns 50, then the monthly investment will be around ₹14,000 if the annual step-up rate will be 10 percent.

So, the investor should keep the annual step-up rate as higher as it's possible for him or her as it curtails monthly investments to a larger extent.

Keep reading our articles for more updates on finance and investment!!

For any kind of query you can contact us at Shri Ashutosh Securities Pvt Ltd., we are here to help you in any way possible.

Happy Investing!

(Mutual Fund investments are subject to market risk Illustrations are for example only, there is no guarantee of returns. Past performance is not an indicator/guarantee to future returns).