Hello Readers!

People when they plan to invest in Mutual Funds, they often land in a problem, how much they should invest or what part of their income is an ideal amount to invest in mutual funds for their goals.

Many financial advisers suggest people should follow the rule of 50*30*20, that is they should use 50% of their salary to cover their monthly and necessary expenses, 30% part of their income they should invest in Mutual funds to grow wealth, and 20% percent they should retain or save, for their wants.

While this 50*30*20 rule can be a good parameter for planning once finance and investment, however, it is always advisable, plan where to invest, how much to invest, and for how much time to invest, based on your goals. Your investment works much better in this way.

Many investors think if they invest a large part of their income in mutual funds, they will be able to get more and more returns. However, this is not the best way to plan your investment, rather the best way to invest is to link your investments to your life goals, your age of investment, your responsibilities, your risk, and other things. In this way, you can plan your investment in the best way.

Here through this article, we are going to illustrate, how you can decide what amount of income is ideal to invest in mutual funds, compatible with your life goals.

Suppose your age is 25 and you are unmarried. At the same time, you have a good six-digit salary, assume Rs 72,000 per month. At this age of yours, you probably have no dependent as you are not married. You have no big responsibilities like wife and children. That means here at this stage of your life you can plan investment for a big part of your investment.

Suppose you planned an amount of Rs 50,000 for investing per month.

Here, at this stage of life, I am assuming three goals for which you may plan to invest.

Goal 1: Rs 10 Lacs that you would require after 5 years to buy a car for yourself.

Goal 2: Rs 2 Cr that you would require after 15 years to buy a house.

Goal 3: Rs 10 Cr that you would require after 35 years for your after-retirement expenses.

Now let us plan your investment for your different goals.

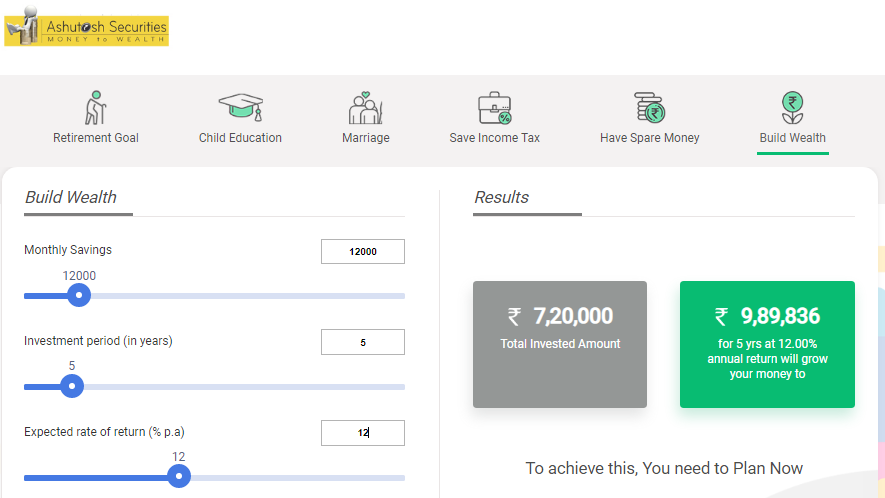

GOAL 1

In order to achieve your first goal, that is to buy a car, you have to plan an investment for five years to build a corpus of Rs 10 lacs. As you are planning for a five-year investment, here you can go investing in Equity mutual funds with a SIP of Rs 12,000, per month.

Now with this portfolio, even with an expectation of a 12% rate of return you can get close to 10 Lacs at the end of 5 years. You can clearly see your investment calculated in the figure below:

GOAL 2

For your second goal, you have to plan your investment for a period of 15 years, this means your investment is going to face a lot of volatilities. You need to stay calm during each volatility and stay invested. You must keep in mind every time that you have a goal associated with your investment which is necessary to be accomplished.

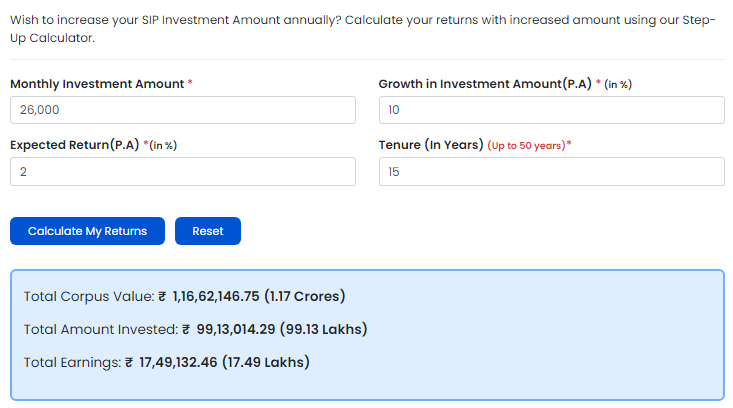

For your second goal, as you have to invest for a period of 15 years, initially you can start your investment in Equity Mutual funds, via a SIP of Rs 26000 per month and then you can go increasing your SIP amount by 10%, every year of your investment till 15 years of investment, through Step-up SIP.

A Step-up SIP means suppose you start investing Rs 26000 per month in the year 2020. From next year you will basically step up your SIP amount by 10% i.e. from 2020 onwards, you will be investing 28600 per month and so on. You can clearly see your investment calculated in the figure below:

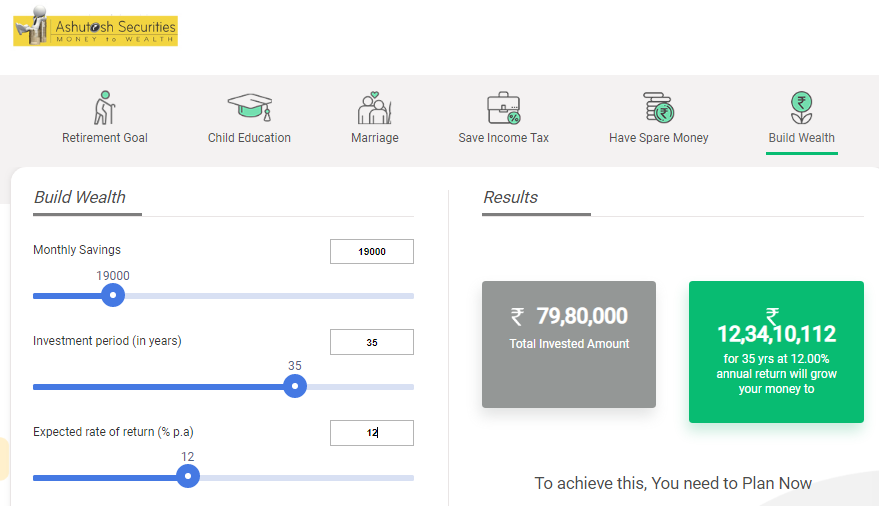

GOAL 3

Your third goal is very much crucial as it is creating a corpus for your retirement, that means along with your today’s expenses, you have to invest for your expenses in later years of your life when you won't have any regular income source.

Assuming, you are going to retire at the age of 60, you will have 35 years to plan your investment for your retirement. First, you need to calculate your monthly expenses after you retire. Taking your current expenses per month as 40k per month, it can be seen that a corpus of close to 10 Cr would be required to fund your retirement.

Also, while planning does not forget, considering the inflation, as inflation can eat into your monthly expenses. If you are spending 40k per month now, at a rate of 6%, that monthly expense figure would grow up to 3.1 lacs after 35 years. Hence, we will have to plan accordingly.

According to this, you would have to start a SIP of Rs 19000 per month, in Equity mutual funds. You can clearly see your investment calculated in the figure below:

Now if we calculate all the SIP then overall, for the 3 goals, you will have to start 3 SIPs (Rs 12000, Rs 26000 and Rs 19000), a total of Rs 57000 in SIPs, which should be sufficient to cover your 3 goals.

That means the amount that we assumed for your investment earlier that is Rs 50,000, that should be increased by more Rs 7,000, to achieve your goals. Alternatively, you can adjust the goal amount and increase/decrease your SIP accordingly.

You might have got a rough idea that there is no ideal amount from your income that can decide to invest in mutual funds. It is your goal and your investment period that decides the ideal amount that you should invest in order to accomplish your goals.

NOTE:

- The above discussion is a basic illustration, how you can plan your investment amount for your different goals. You might go doing changes in numbers, according to your expenses, as with the increasing age, your responsibilities and income both have a growth trend.

- The returns shown in the figures are calculated by the SIP calculator, and they are not actual returns, instead, they are expected returns. Actual returns may differ.

For any kind of query, you can contact us at Shri Ashutosh Securities Pvt Ltd., we are here to help you in any way possible.

Happy Investing!

(Mutual Fund investments are subject to market risk Illustrations are for example only, there is no guarantee of returns. Past performance is not an indicator/guarantee to future returns).